Crypto lending is the practice of borrowing money against cryptocurrency you already own, instead of selling it. You pledge an asset like Bitcoin as collateral, receive cash — usually a stablecoin such as USDC — and repay the loan plus interest over time. When you repay in full, your collateral is returned. It is the crypto equivalent of a home-equity line of credit: your asset keeps working for you while you unlock liquidity from it.

This guide explains how crypto lending actually works in 2026, the key terms you need to understand, the critical difference between custodial and non-custodial models, and how marketplace platforms like Coinedge fit into the picture.

Why borrow against crypto instead of selling?

Selling Bitcoin to raise cash has two big drawbacks: you give up future upside if the price rises, and in many jurisdictions a sale is a taxable disposal. Borrowing against your BTC lets you access dollars while keeping your position. For long-term holders who believe in the asset but need short-term liquidity, that trade-off is often far more attractive than selling.

- Keep your Bitcoin exposure — you still benefit if the price goes up.

- Avoid triggering a taxable sale just to access cash (consult a tax professional for your situation).

- No credit check — your collateral, not your credit score, underwrites the loan.

- Use the cash for anything: expenses, investments, or bridging a short-term gap.

The core mechanics: collateral, LTV, and repayment

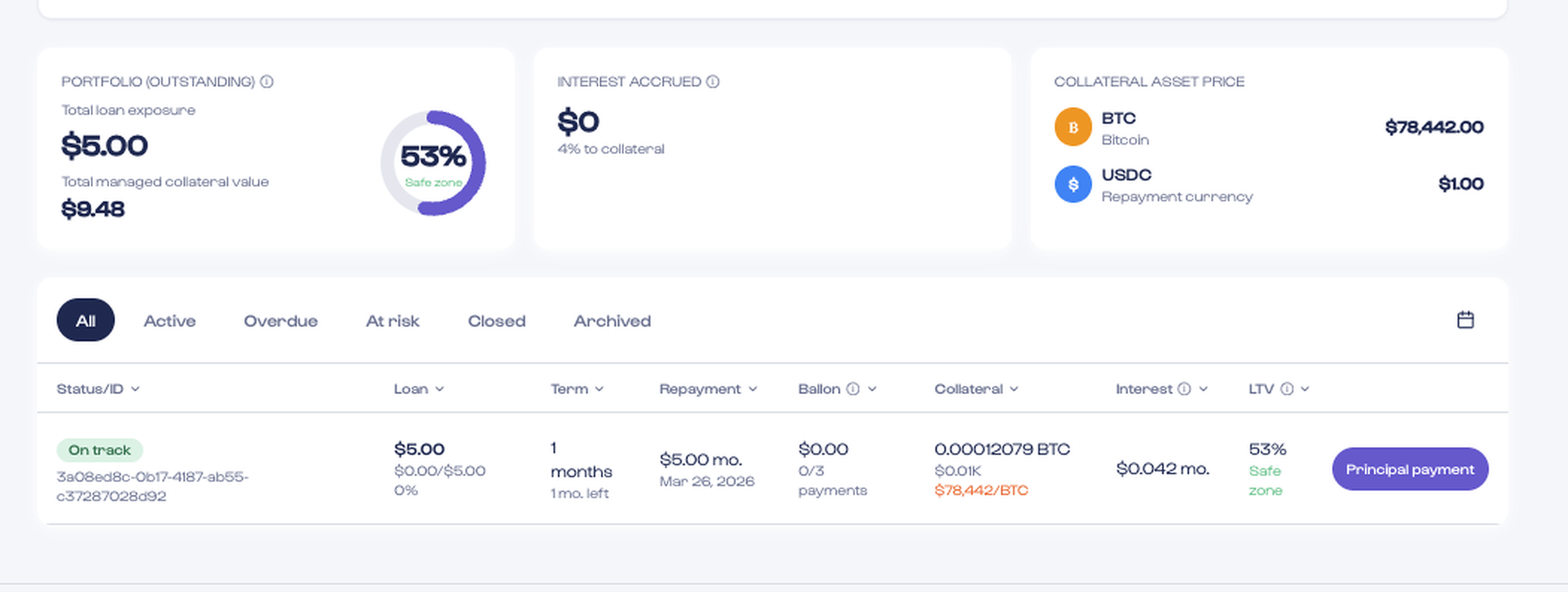

Every crypto loan revolves around three numbers: how much collateral you post, how much you borrow against it, and the interest rate. The relationship between the loan and the collateral is captured by the loan-to-value ratio, or LTV.

LTV is the loan amount expressed as a percentage of your collateral's value. Borrow $6,000 USDC against $10,000 of Bitcoin and your LTV is 60%. Because Bitcoin's price moves, your LTV moves with it: if BTC falls, your LTV rises and your loan becomes riskier. We cover this in depth in What Is LTV in Crypto Lending?.

Overcollateralization keeps loans safe

Crypto loans are overcollateralized — you always pledge more value than you borrow. That buffer protects the lender against price swings and is the reason BTC-backed loans require no credit check.

Custodial vs non-custodial: the most important distinction

This is the single most important thing to understand before choosing a platform. In a custodial model, you hand your Bitcoin to the lender, who holds it in their own wallet. You are trusting them not to lose it, re-lend it, or freeze withdrawals. The 2022 collapses of BlockFi, Celsius, and Voyager were all custodial lenders — when they went under, customers' coins were trapped in bankruptcy.

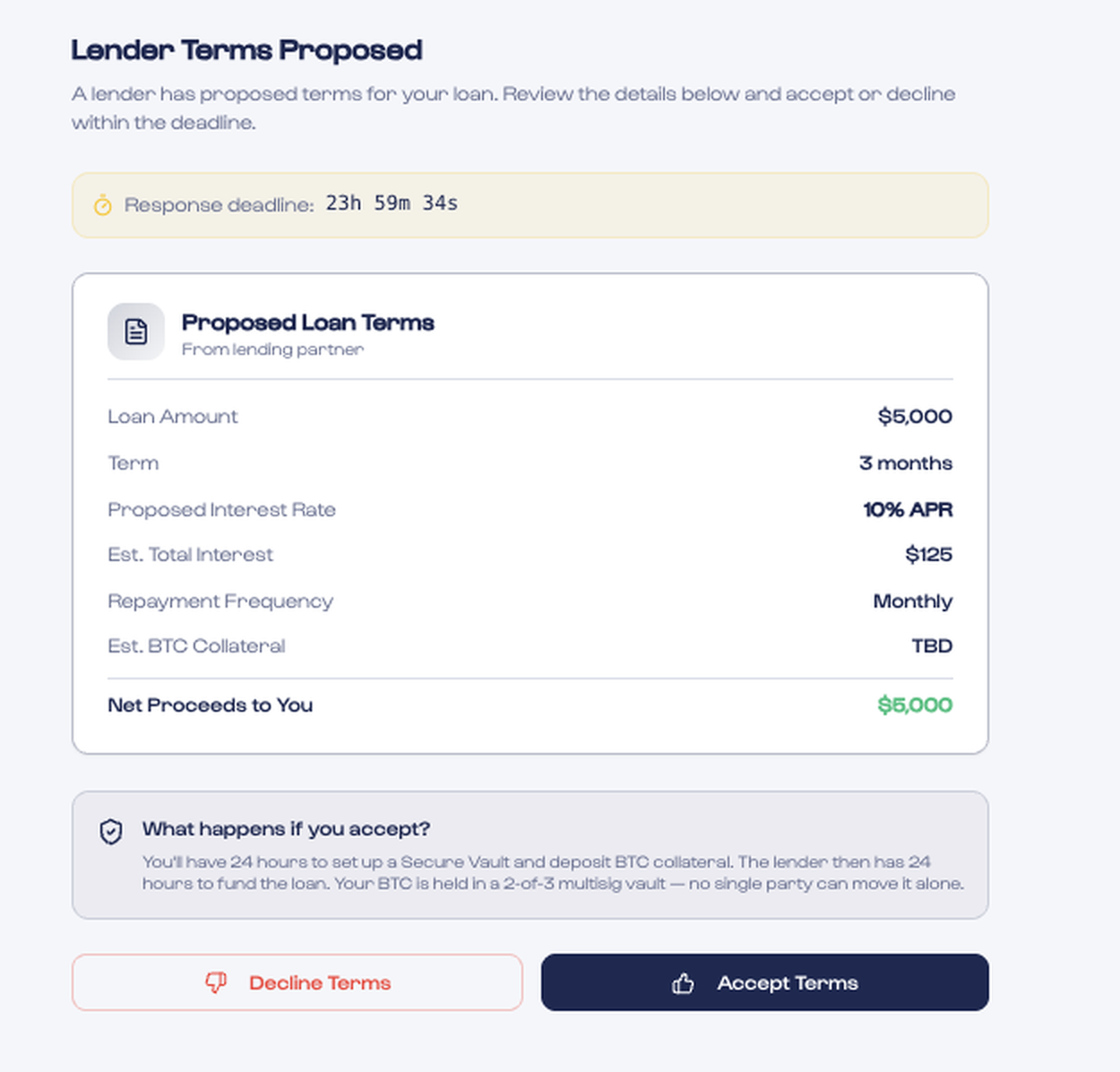

In a non-custodial model, no single party ever controls your Bitcoin. Coinedge uses a 3-key multisig vault where the borrower, the lender, and Coinedge each hold one key, and all three signatures are required to move funds. The collateral can never be re-lent or rehypothecated. We explain the architecture in 3-Key Multisig Explained.

Where marketplaces fit in

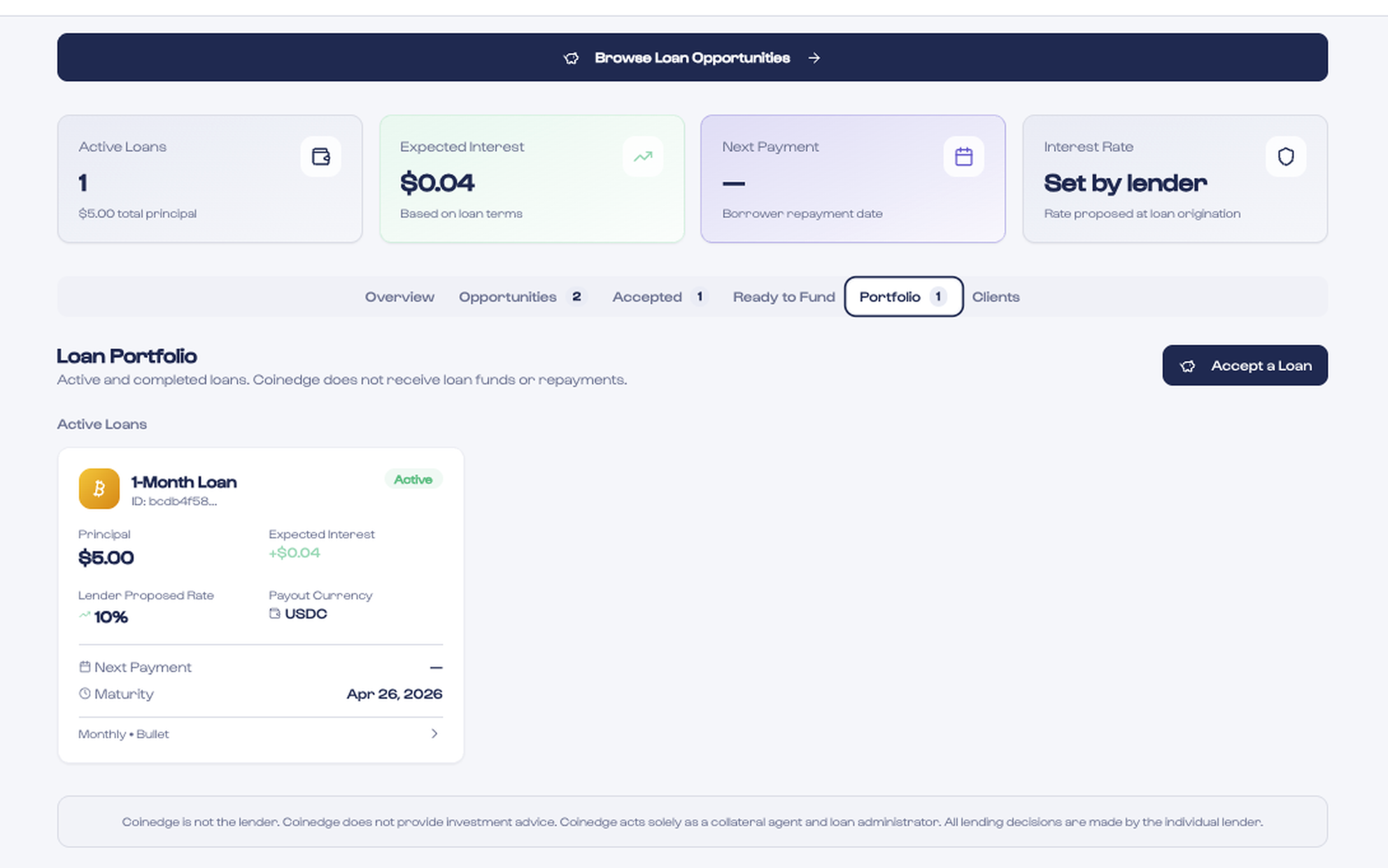

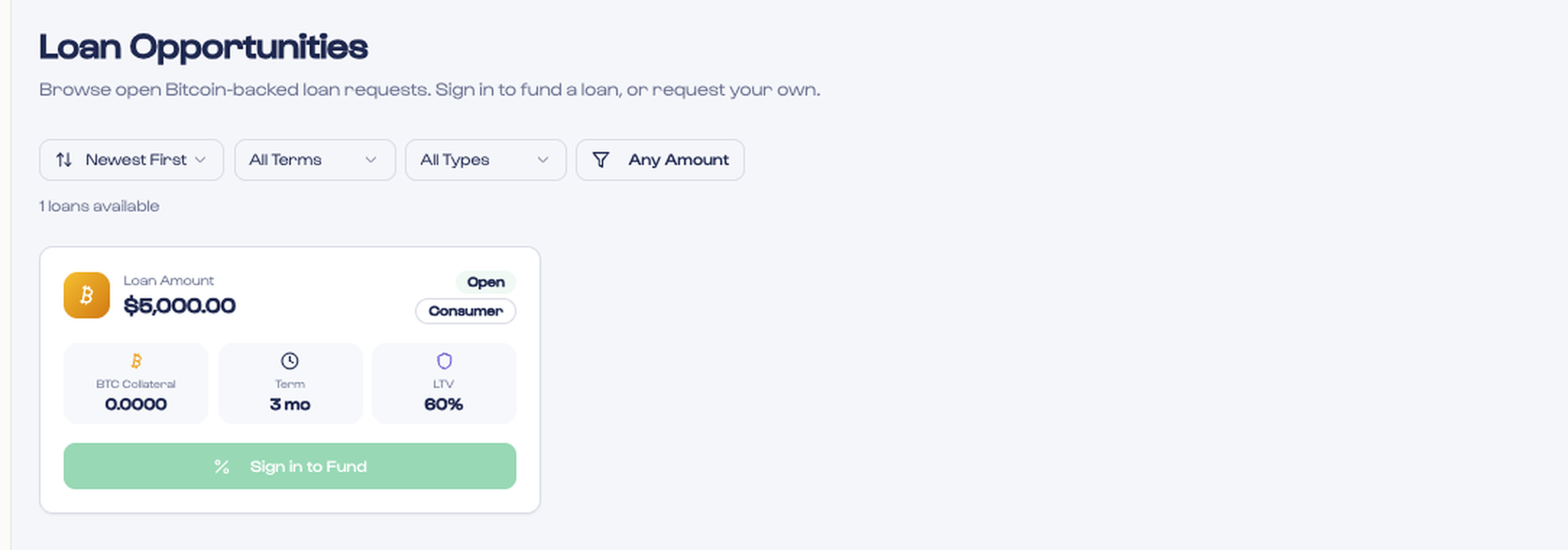

Most early crypto lenders were balance-sheet lenders: the company itself lent you its money and set the rate. A marketplace works differently. Coinedge does not lend its own money or set rates — it connects borrowers who want liquidity with independent lenders who compete to fund loans. Borrowers receive competing rate proposals; lenders choose which requests to fund. The platform's job is coordination and collateral security, not being the counterparty.

If you want to access cash, start on the borrow page. If you have capital to deploy and want to earn yield on overcollateralized BTC loans, see how lending works.

Is crypto lending safe?

It depends entirely on the model. Custodial lending carries counterparty risk — you are exposed to the platform's solvency. Non-custodial lending removes that risk by ensuring no one can touch your collateral unilaterally. The remaining risk for borrowers is price volatility: if Bitcoin drops sharply, you may need to add collateral or repay early to avoid liquidation. Understanding LTV thresholds before you borrow is essential.