Liquidation is the single risk every Bitcoin borrower must understand before taking a loan. It is what happens when your collateral can no longer safely cover what you owe — usually because Bitcoin's price has fallen far enough that your loan-to-value ratio breaches a pre-agreed threshold. The good news: liquidation is almost always avoidable if you understand how it works and borrow sensibly.

What triggers liquidation

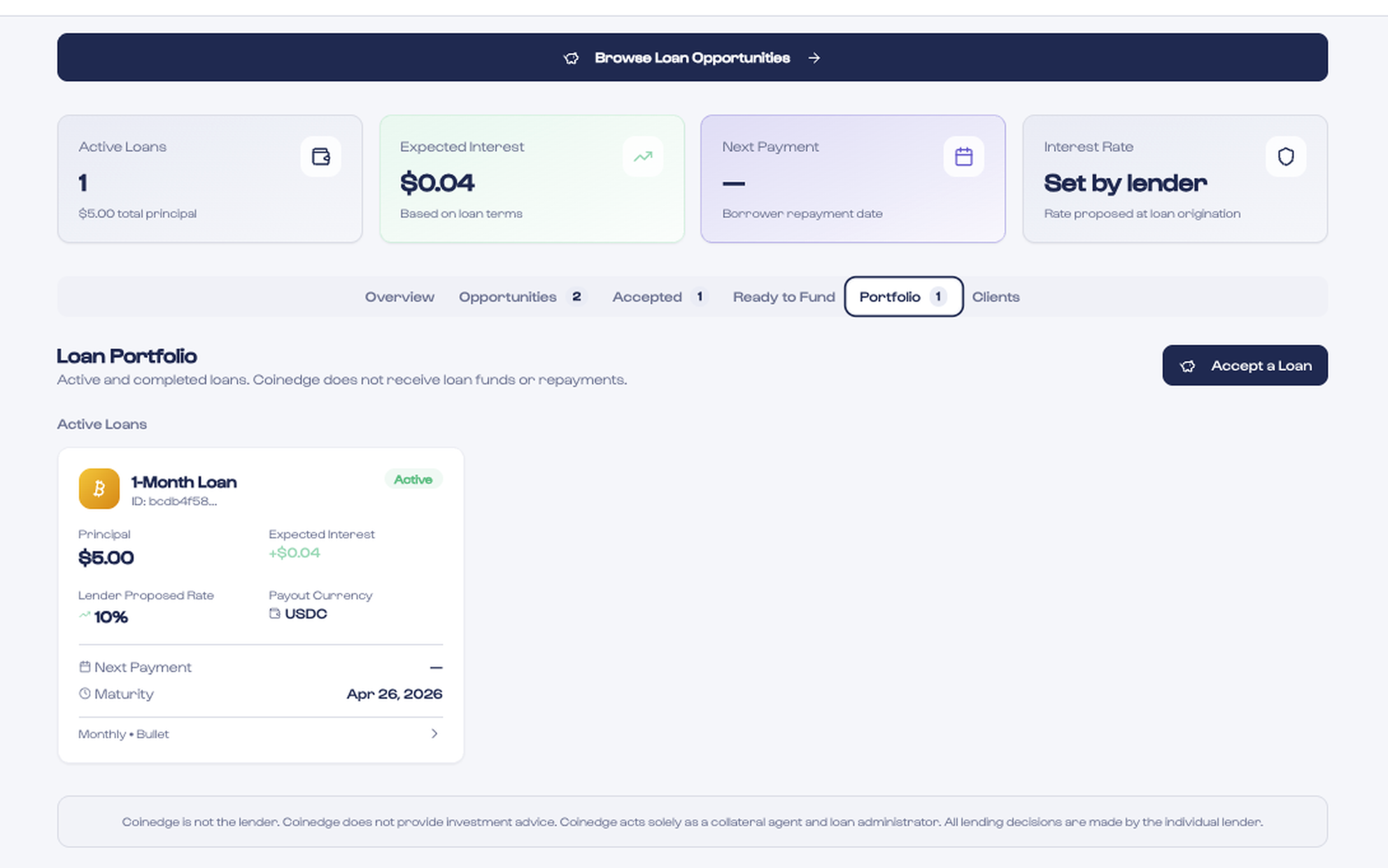

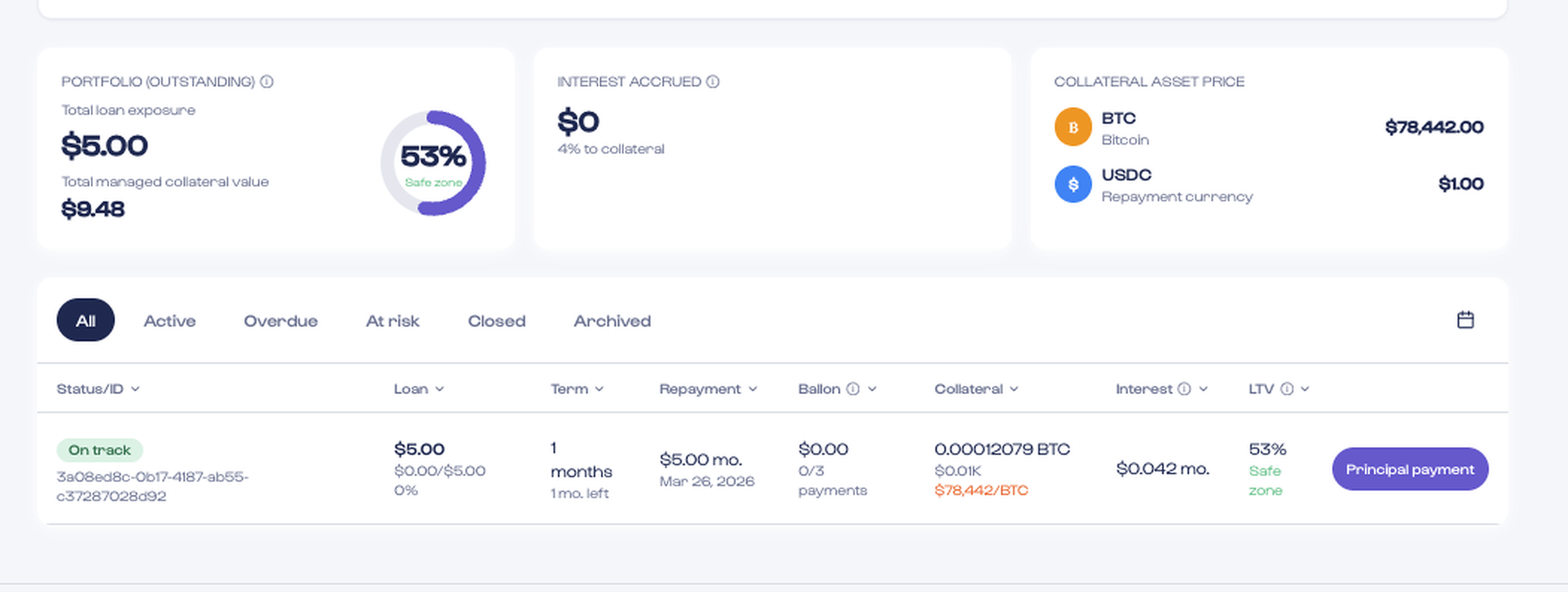

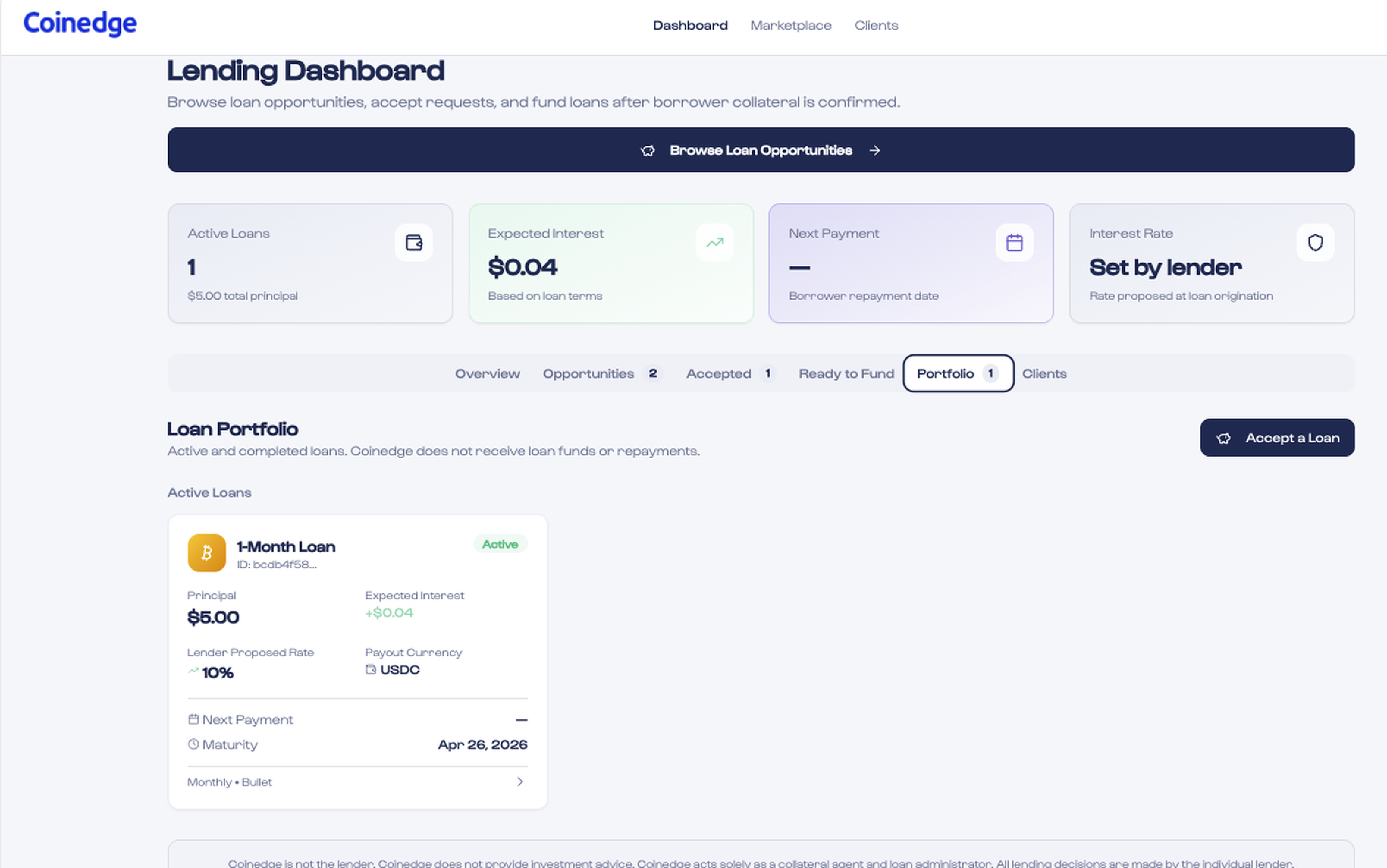

Every loan is overcollateralized, meaning you pledge more value than you borrow. As Bitcoin's price moves, your loan-to-value (LTV) ratio moves with it. If BTC falls enough that your LTV climbs toward the liquidation threshold set at origination, the loan is at risk. If the threshold is breached and you take no action, collateral is sold to repay the lender. We explain the math in What Is LTV in Crypto Lending?.

A simple example

Borrow $5,000 against $10,000 of BTC (50% LTV) with a 75% liquidation threshold. If Bitcoin falls about 33%, your collateral drops to ~$6,650 and your LTV rises to ~75% — the danger zone.

What actually happens to your Bitcoin

Before liquidation, you are warned. As your LTV approaches the threshold, you receive alerts and a chance to act. Only if no action is taken and the threshold is breached is collateral sold — and only enough to bring the loan back to a safe state and repay the lender per the agreed terms. On Coinedge, this happens through the pre-agreed multisig workflow, not by any single party seizing your coins. See 3-Key Multisig Explained.

How to avoid liquidation

- Borrow at a conservative starting LTV — many borrowers target 30–50% for a bigger cushion.

- Keep some spare BTC ready so you can top up collateral quickly if prices fall.

- Make an early partial repayment to lower your LTV when the market gets volatile.

- Watch your portfolio dashboard and respond to margin alerts promptly.

- Choose a shorter term or smaller loan if you expect volatility.

The biggest lever is your starting LTV

A loan that starts at 30% LTV can withstand a much larger Bitcoin drop before reaching liquidation than one that starts at 60%. Conservative borrowing is the simplest protection.

Want to see how different loan sizes and LTVs behave? Try the Bitcoin loan calculator or the loan-to-value calculator, then start a request on the borrow page.