Not legal or financial advice

This article is general education, not legal or tax advice. Regulation varies by state and changes frequently. Consult a qualified attorney or compliance professional about your specific situation.

Crypto lending regulation in the United States looks very different in 2026 than it did during the 2020–2021 boom. The collapses of BlockFi, Celsius, Voyager, and Genesis triggered a wave of enforcement and reshaped how regulators think about who is allowed to lend, what disclosures are required, and — most importantly — who controls customer assets. This guide explains the landscape in plain English.

What went wrong in 2022

The lenders that failed in 2022 shared a common structure: they were custodial. Customers handed over their crypto, and the platform pooled it, re-lent it, and in some cases used it for proprietary trading. When markets turned, those platforms could not meet withdrawals, and customers became unsecured creditors in bankruptcy. Regulators concluded that many of these products were effectively unregistered securities offerings.

The regulatory response

Since then, US regulators have focused on several themes. Borrowers and lenders should understand each:

- Securities treatment: Pooled, interest-bearing crypto accounts have repeatedly been treated as securities requiring registration and disclosure.

- Custody and consumer protection: Regulators scrutinize whether a platform takes custody of customer assets and how those assets are safeguarded.

- State money-transmission and lending licenses: Many states require licensing for entities that lend or transmit funds.

- Disclosure standards: Clear, accurate disclosure of risk, rates, and the platform's role is increasingly expected.

Why the custodial vs non-custodial distinction matters legally

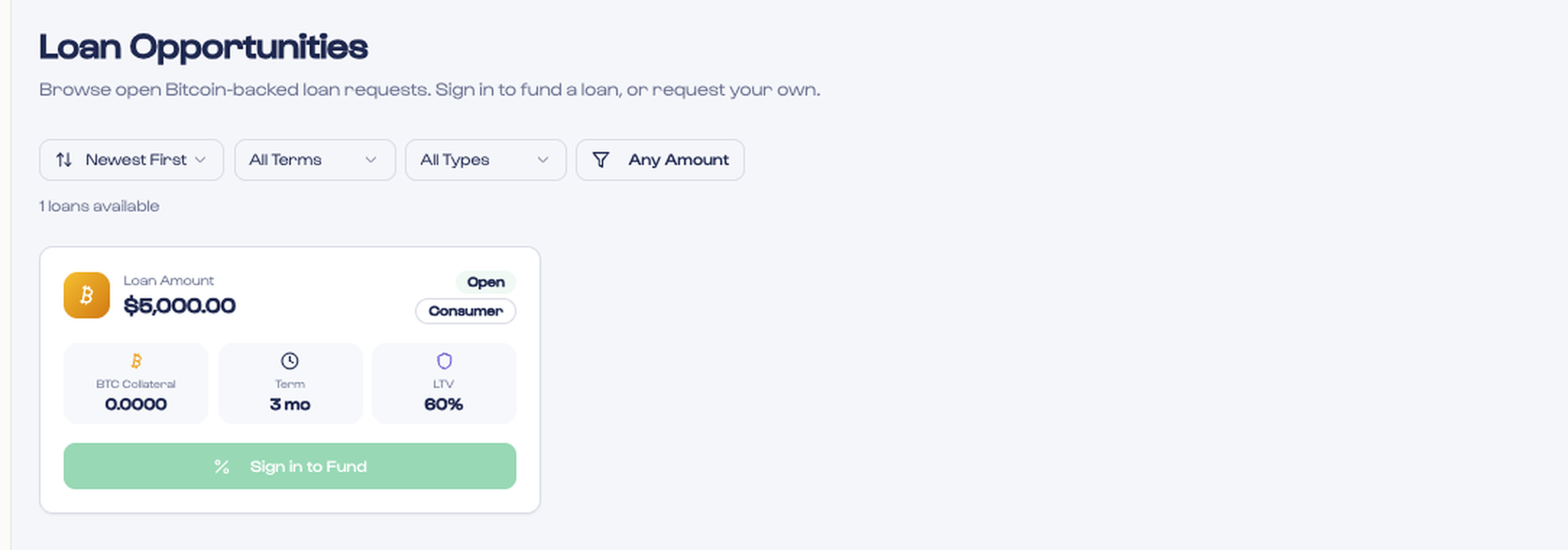

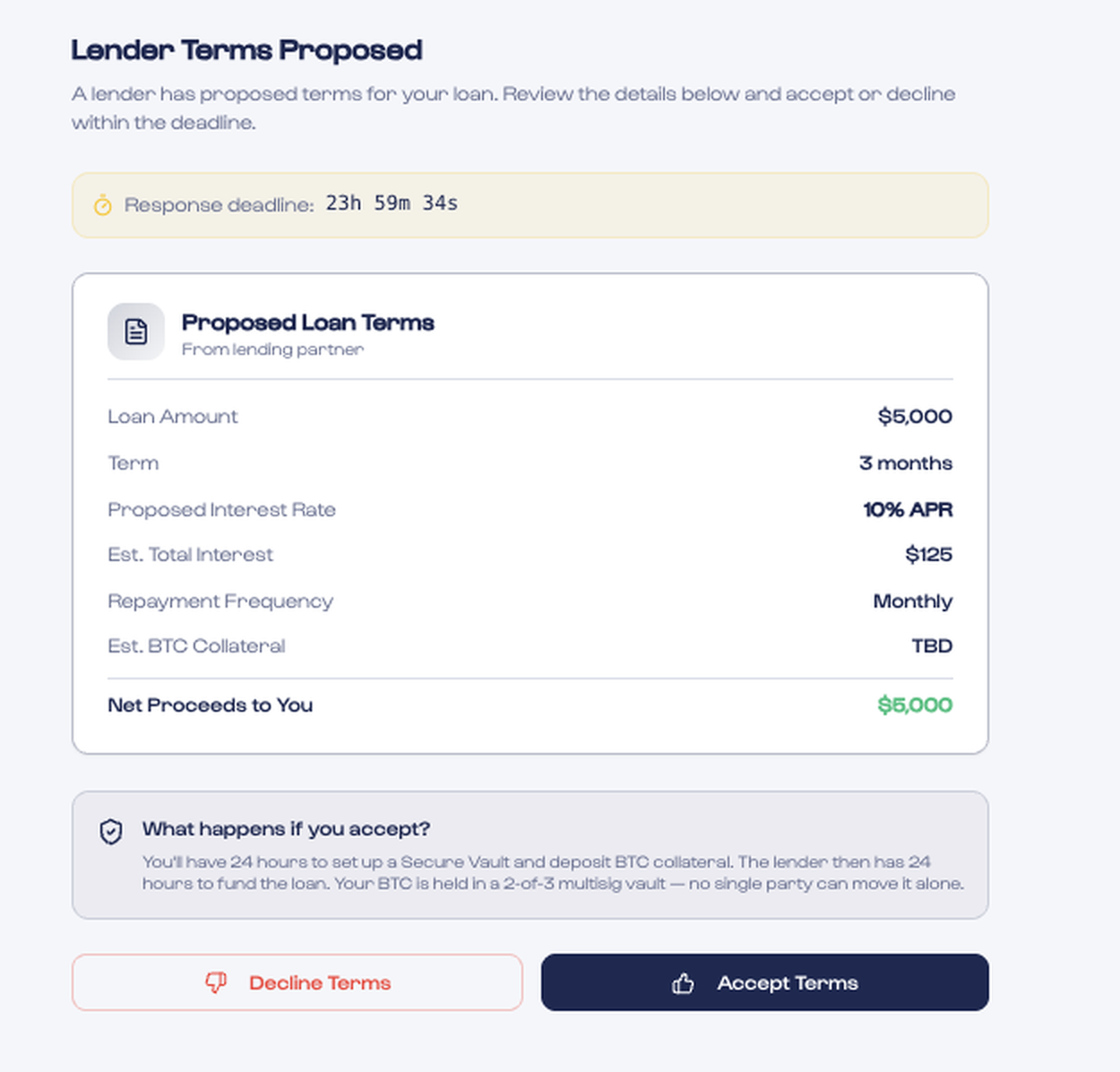

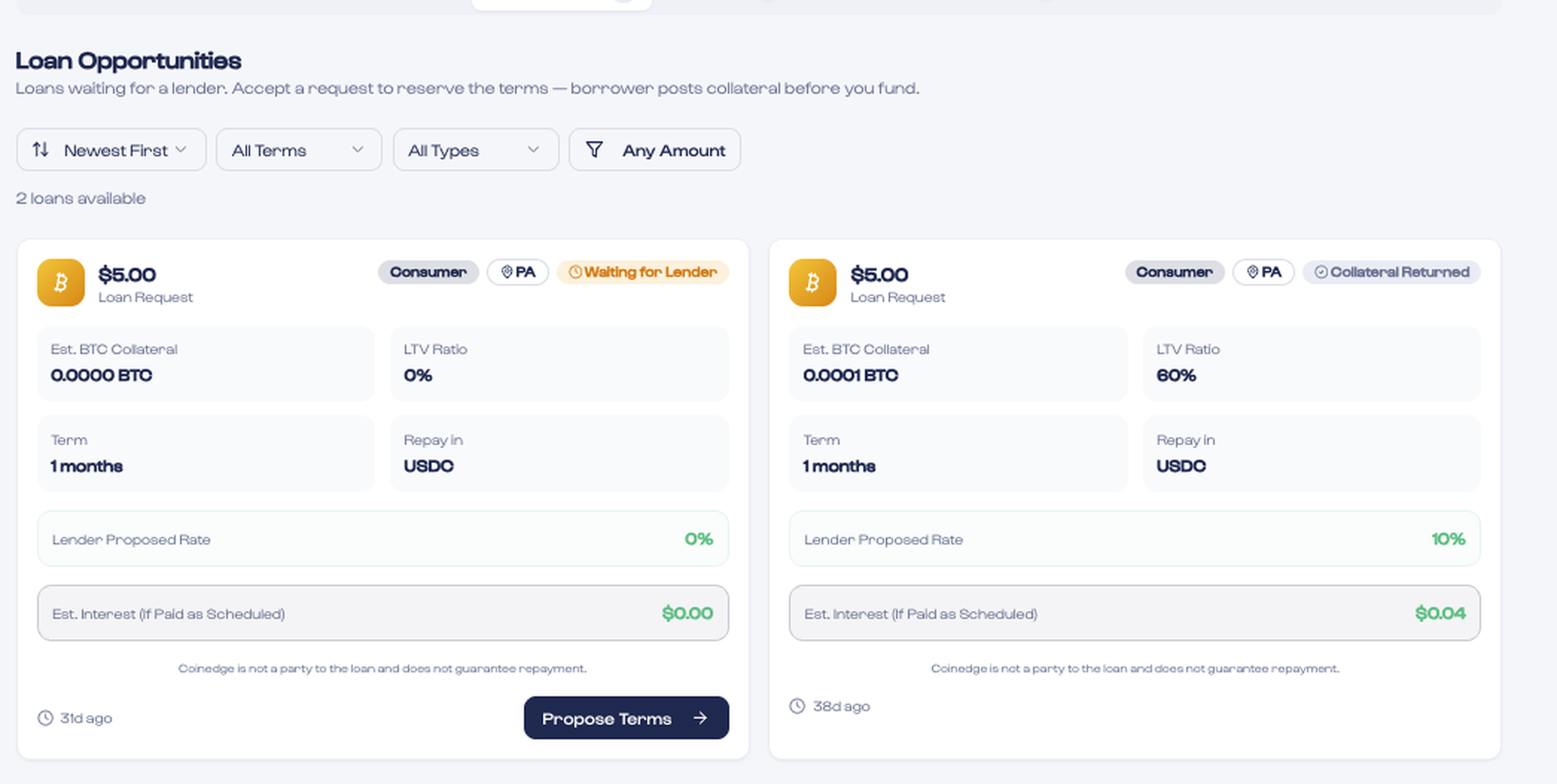

The biggest regulatory and consumer-protection question is custody. A custodial lender holds and controls your assets — which is precisely what created systemic risk and consumer harm in 2022. A non-custodial model where collateral sits in a multisig vault that no single party controls fundamentally changes the risk profile: there is no pool of customer assets for a platform to misuse, and there is no single point of failure. We explain that architecture in 3-Key Multisig Explained.

How a non-custodial marketplace is structured

Coinedge operates as a marketplace and collateral agent, not a balance-sheet lender. It does not take custody of Bitcoin, does not pool customer funds, does not set interest rates, and does not receive or hold loan proceeds — USDC flows directly between lender and borrower wallets. This separation of roles is designed precisely around the lessons of the last cycle. You can read more on the security page.

What borrowers should check

- Does the platform take custody of your collateral, or is it held in a vault no single party controls?

- Is your collateral ever re-lent or rehypothecated?

- Are the terms, fees, and liquidation rules clearly disclosed before you commit?

- Who actually sets the interest rate — the platform, or independent lenders?

What lenders should check

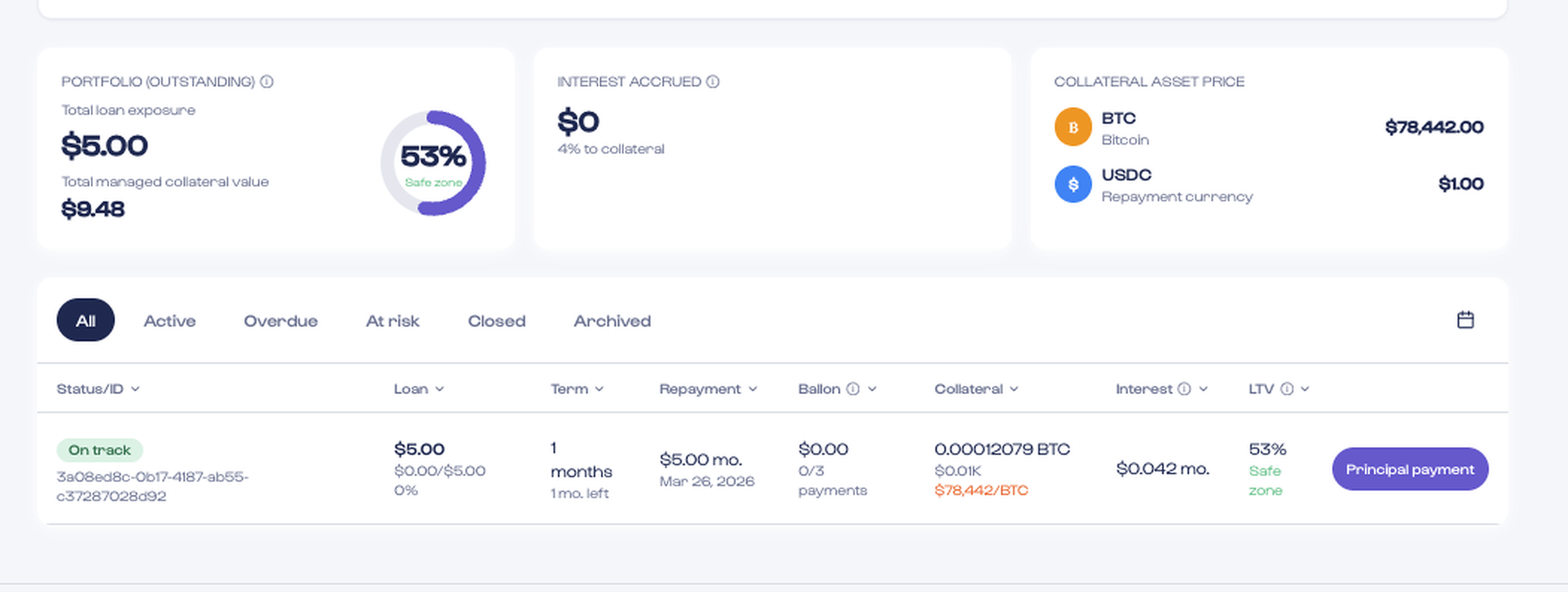

- Is the loan overcollateralized, and what is the liquidation threshold?

- How is collateral secured and who holds the keys?

- What is the platform's role if a borrower defaults?

- Are you lending to the platform, or directly to borrowers?

Want the fundamentals first? Start with What Is Crypto Lending?. Ready to participate? See the borrow and lend pages.